Thank you Plevey. I realise that my situation is different to many because it was bereavement which changed my plans rather than equalisation.

I don’t recall when it was that I became aware that the letter the Pension Service sent me was wrong but probably by 2011 at the latest.

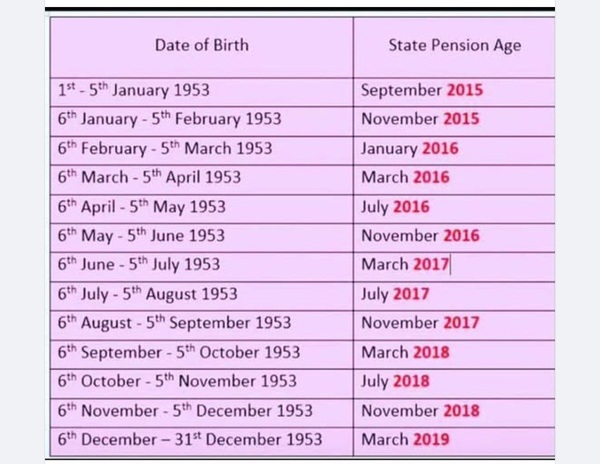

The Pension Act 2007, which increased the SP age to 66, was passed on 26 July 2007 which was only four months after DH died, when I was trying to juggle being back at work and dealing with his estate. The latter meant winding up a business as well as his personal estate. It was a time when, best will in the world, my brain would not have been functioning at its best. I may have been vaguely aware that SP age was increasing to 66 but as it was going to happen between 2024 and 2026, long after I turned 60, I probably thought it didn’t apply. Anyway, the Pension Service took a long time to process my claim for Bereavement Allowance and the letter telling my SP age was 60 came after that Act was passed. One doesn’t automatically think that a government letter is giving false information.

I think I must have been aware by 2011, when George Osborne accelerated the changes, just four years short of when I had expected to receive my SP. I keep meticulous records and certainly never received any letter from the DWP.

The 2024 PHSO report Annex A says my cohort (dob 6 April 1955 to 5 April 1960 of women affected by the Pensions Acts 1995 and 2011, were sent letters between October 2012 and November 2013 (including a pause from January to May 2013). 4,475,000 million letters were alleged to have been sent but paragraph 89 of the 2021 PHSO report says DWP does not have a record of who it wrote to.

I’m not expecting compensation. Here’s the PHSO’s Summary of the levels of injustice and ranges of compensation in our severity of injustice scale - see Annex C here:

www.ombudsman.org.uk/sites/default/files/Women%E2%80%99s-State-Pension-age-our-findings-on-injustice-and-associated-issues.pdf

As most, I might fall into Level 2 and be paid £100 to £450. I’m annoyed that the Pension Service sent me wrong information and the letter allegedly sent in 2012 or 2013 was not received but it’s relatively low impact injustice. I had a well paid job and a good pension scheme and also receive widow’s pensions from the schemes my DH paid into, so I could not by any stretch claim hardship. Had he lived, his SP age would not have been altered by the 2011 Act but mine was. Nevertheless, I have “lost” around £40,000 as a result of equalisation, income we were expecting to have and would have taken into account in our planning in the mid 2000s. Would we have changed our plans if we had realised I would not be getting my SP at 60? Probably not as we had good workplace pensions and other assets.

And there’s the crux. Of over 3 million women affected by equalisation, everyone’s case is different and DWP are never going to review them all. Looking at Annex C, I doubt many could make a case for the higher levels of compensation which at level 6 is only £10,000 roughly the equivalent of one year of pension.

As things turned out, I could argue that I was worst affected by the abolition of the State Widows Pension in 2001. Had that not been abolished I would have received a State Widows Pension (albeit reduced as I was under 55 when widowed) from 2007 until I finally reached State Pension age in 2021. That’s 14 years loss of pension. But then I accept that too, in the same way that I accept equalisation. It was a move away from inherited state pensions because by 2001 most married women now worked outside the home, had their own income and built their own pensions. Widows were now expected to work or continue to work after a major life change just as separated and divorced women are expected to do, rather than rely on state support.

The irony is that when MPs were debating the abolition of State Widows Pension, Hansard shows that it was to put the money saved into the old age pension, which for women and later men, was now going to be further away.

The bottom line is that State Pension rights are being eroded bit by bit for everyone. The point of the introduction of the single tier State Pension from 6 April 2016 was to make it cheaper per capita to pay in the long term. Less variable Additional State Pension to pay as older pensioners who paid into SERPS/SSP die and are replaced by younger pensioners with no SERPS/SSP. But it’s going to take another 20 years or so for most people with aSP or Protected Payments to die. Meantime record numbers of people are reaching State Pension age due to the baby boom of the 1950s and 1960s.

It would nice if the government were to make some financial gesture in recognition that they did maladminister equalisation, not least that James Purnell, who seems to be Burnham's pick for Chief of Staff, was in post at the DWP when the worst of the maladministration was happening but I doubt many women would be happy with what was offered.